Car insurance plans are essential for every vehicle owner. A car insurance plan protects you financially in case of accidents, theft, or damage. With the right plan, you cover medical bills, repairs, and liability costs. Because most states require auto insurance, choosing the right coverage is crucial. In recent years, premiums have risen sharply. The average U.S. auto premium is now about $1,759 per year. That’s why understanding and comparing car insurance plans can save you hundreds or even thousands of dollars.

Figure: A car insurance policy document with a magnifying glass and a model car on the table, symbolising the importance of reviewing your car insurance plan in detail.

Our guide will explain Car Insurance Plans in depth, including coverage options, how rates are determined, tips for affordable quotes, and more. We’ll also address commonly confused terms (such as healthcare plans vs. car insurance). By the end, you’ll know how to compare plans, use discounts, and choose coverage that fits your needs—car insurance plans.

Understanding Car Insurance Plans?

A car insurance plan (or auto insurance policy) is a contract between you and an insurer. You pay a premium, and in return, the insurer covers certain costs if you are involved in a covered incident. Most plans are annual policies that renew every year. Standard car insurance coverages include liability, collision, and comprehensive.

All drivers must meet their state’s minimum requirements, which usually include liability insurance. Some states (no-fault states) also require personal injury protection. Beyond legal minimums, many drivers add extra coverages for more protection. For example, roadside assistance or rental reimbursement can be add-ons to a car insurance plan.

Your Car Insurance Plan includes coverage limits, deductibles, and optional add-ons. Deductibles are what you pay out-of-pocket before insurance kicks in, so choosing the right deductible affects your premium. Lower deductibles mean higher premiums, and vice versa. Reviewing policy terms (coverage limits, exclusions, deductibles) is essential so you know exactly what is covered.

In short, a car insurance plan ensures you’re covered against losses related to your vehicle. It’s not to be confused with health insurance—for example, “Affordable Care Act insurance plans” refer to health policies, not auto policies. Similarly, terms like “Florida Health Care Plan insurance” or “Fidelis Care insurance plans” refer to medical coverage, not auto insurance. In this article, we focus only on car/auto insurance plans.

Key Types of Auto Insurance Coverage?

Car insurance plans usually include several types of coverage. Understanding each helps you pick the right plan. Here are the main types:

- Liability Coverage: Covers damage/injury you cause to others. Includes Bodily Injury Liability (medical costs if you injure someone) and Property Damage Liability (repairs to other vehicles or property). Every plan should have at least the state-required liability coverage.

- Collision Coverage: Pays for damage to your car if you hit another vehicle or object (like a tree). This coverage kicks in after your deductible. Useful even if you’re at fault, as it handles your car’s repair costs.

- Comprehensive Coverage: Covers non-collision damage to your car – for example, theft, vandalism, natural disasters (hail, flooding), or hitting an animal. Again, you pay a deductible, then insurance covers the rest.

- Uninsured/Underinsured Motorist Coverage (UM/UIM): If you’re in an accident with a driver who has no insurance or insufficient insurance, UM/UIM covers your expenses (medical or car repair). This protects you against reckless drivers who lack proper coverage.

- Medical Payments (MedPay) / Personal Injury Protection (PIP): Pays for medical bills for you and your passengers, regardless of fault. PIP can also cover lost wages. Some states require PIP (no-fault) car insurance plans.

Each coverage type comes with limits. For instance, a plan might have $50,000 per person bodily injury and $100,000 per accident. You choose these limits based on your needs and budget.

Liability Coverage

Liability is mandatory in most states. It only covers others’ losses, not your own. Example: If you rear-end someone, your liability insurance pays for their car repairs and medical bills, up to your policy limits. If damages exceed your limits, you’d pay the rest out-of-pocket.

Tip: Even if state minimums are low (e.g. $10,000), consider higher limits. Many experts advise at least $50K/$100 (per person/per accident). Higher coverage costs slightly more, but protects you from lawsuits.

Collision Coverage

This covers your own vehicle’s damage in a crash. You pay the deductible, then the insurer pays the rest (up to the car’s value). For example, if you have a $500 deductible and $2,000 collision claim, you pay $500, and the insurer pays $1,500.

If your car is older or low-value, you might skip collision coverage to save money. However, without collision, you’d pay all repair bills after an accident. Weigh the car’s value vs the premium difference when deciding on collision coverage.

Comprehensive Coverage

Comprehensive kicks in for non-crash losses. Typical scenarios: hail damages your windshield, your car is stolen, or a tree branch falls on your roof. Comprehensive also has a deductible. For $

1000 damage and a $250 deductible, insurance pays $750.

If you live in an area prone to theft, storms, or wildlife collisions, comprehensive coverage is advisable. As with collision, older cars might not be worth the extra premium if the car’s value is low.

Uninsured/Underinsured Motorist Coverage?

UM/UIM protects you when the at-fault driver lacks insurance or has too little. State laws vary in requirements. But adding UM is generally inexpensive and valuable. According to Car and Driver, “almost all insurance companies provide roadside assistance as optional coverage” (roadside assistance is similar to optional coverage). By analogy, UM coverage is also usually optional but highly recommended.

Example: If a hit-and-run damages your car, UM can cover repairs. Or if the other driver’s liability maxes out, your UM kicks in—car insurance plans.

Medical Payments / PIP

This covers your medical bills and your passengers’ medical bills, regardless of fault. It’s like mini-health insurance for car accidents. PIP goes beyond medical, sometimes covering lost wages. States like New York or Florida often require PIP. If you already have good health insurance, MedPay might be less critical. But PIP can still cover deductibles and co-pays from your health plan after a crash.

Key Point: Always check state laws. For instance, Florida has “Florida Personal Injury Protection (PIP)” rules. Medical coverage in car insurance is different from Florida’s health insurance programs. Confusion can arise: “Florida Health Care Plan insurance” is a healthcare program, not an auto insurance program. Our focus is auto insurance – all coverages here pay out for vehicle-related incidents.

Factors Influencing Car Insurance Premiums?

Your monthly or annual premium depends on many factors. Here are the big ones:

- Vehicle type and usage: Expensive or high-performance cars cost more to insure. Low safety ratings, expensive repairs, or fast models increase premiums. For example, Progressive notes that insuring a car over $150,000 often requires a speciality insurer. How much you drive matters too – more miles mean a higher chance of accidents, leading to higher rates.

- Driver profile: Age, gender, driving record, credit score, and experience all matter. Teen drivers pay far more than adults. According to a recent study, a 16-year-old on a parent’s policy could save about 10.9% (around $546) on premiums if they qualify for a good student discount. In general, drivers with clean records and good grades get deals, while DUIs or accidents raise rates.

- Location: Where you live and where you drive are huge. Urban areas with more traffic or higher theft/vandalism risk have costlier insurance. The Zebra reports that Michigan has the highest monthly premiums ($211) and Florida is the second-highest ($194). (This reflects car insurance, not Florida health plans.) Premiums vary widely: cheapest states like Maine average $935/year, while busy cities can exceed $6,000/year. Always consider local rates.

- Coverage limits and deductibles: Higher coverage limits cost more. Lower deductibles (meaning insurer pays more after a claim) also raise premiums. If you opt for minimal coverage to save money, you risk enormous out-of-pocket costs in a claim.

- Credit score: In many states, insurers use your credit-based insurance score. Better credit often means lower rates.

- Annual mileage: Some companies offer usage-based plans or pay-per-mile programs. If you drive very little, you might get a discount. Conversely, long commutes bump up premiums.

Each insurer weighs these factors differently. That’s why comparing quotes is vital – one company may favour certain factors over another, so a quote from one insurer could be 20% lower than another even for the same coverage.

Vehicle and Usage

Insurance companies classify cars by risk. A family sedan is usually cheaper to insure than a sports coupe. High repair costs (luxury brands, imported parts) and high theft rates (some models are targets for thieves) increase premiums. Additionally, how you use the car matters; a car used only for errands may be cheaper than one used for a 50-mile daily commute.

Remember, for very expensive or classic cars, standard car insurance plans might not cover agreed value. Some owners get classic or agreed-value insurance to ensure a set payout. These are like luxe car insurance plans tailored for luxury vehicles.

Driver Profile

Younger drivers pay more. According to data, younger drivers (especially teens) can have average annual premiums in the thousands. However, discounts exist. A good student discount can save young drivers about 10.9% on average. If a student maintains a B average or above, insurers may knock off part of the premium.

On the other hand, negative marks like DUIs, speeding tickets, or accidents can skyrocket your rate. For example, a DUI can increase premiums by 80% or more. Safe driver discounts (no tickets/claims) can reduce rates. Insurers also offer discounts for defensive driving courses or for vehicles with safety features (such as anti-theft devices, airbags, and anti-lock brakes).

Location

Where you live and where you park your car play a significant role. The Zebra’s data shows state-by-state differences. For instance, Florida’s high accident rates and legal climate keep premiums high ($194/month on average). In contrast, a state like Maine averages only $935/year. Even within a state, city vs rural rates differ. High-crime areas or dense cities often pay more.

Note: “Florida health care plan insurance” does not affect auto insurance, but Florida’s auto insurance rules and risk factors do. Florida used to have no-fault PIP laws, which made insurance more expensive (though recent changes have reduced costs). When comparing plans, consider both state requirements and local risk factors.

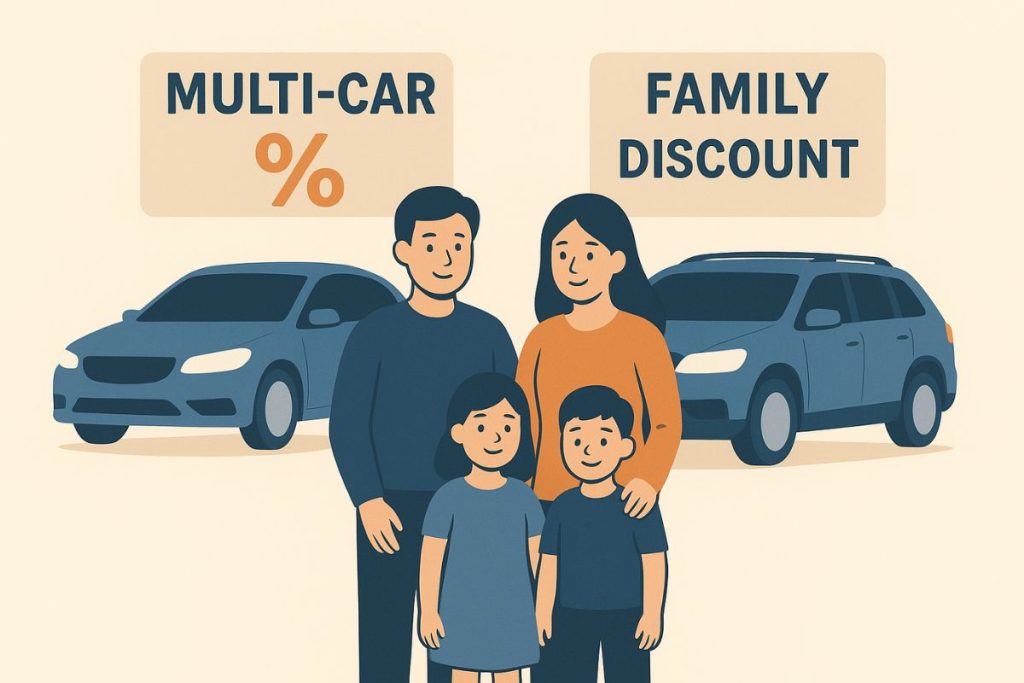

Discounts and Bundling

Most insurers offer multiple discounts. Common ones include:

- Multi-car/Family Policy Discount: Insuring two or more vehicles on one policy usually earns a multi-car discount. Progressive, for example, explicitly states you “can earn a multi-car discount when you have more than one vehicle listed on your policy”. Usually, adding a spouse or child to a car qualifies.

- Multi-policy Discount: Bundling auto with home/renters or other insurance typically lowers rates. Many insurers will cut 10-20% if you buy, say, auto + homeowners from them.

- Good Student Discount: As noted, students with good grades save (10-15% on average).

- Low Mileage Discount: Driving fewer than 7,500 or 10,000 miles/year can earn a lower rate.

- Safety Features: Cars with airbags, anti-lock brakes, anti-theft devices, or backup cameras may get discounts.

- Pay-in-Full Discount: Some carriers offer a discount on the annual premium if you pay the premium up front rather than in monthly instalments.

A family car insurance plan often combines multi-car and safe-driver discounts. For example, if you insure two cars (parent + teen) on one policy, both vehicles may qualify for a “multi-car discount” and possibly a “good student” discount for the teen.

Example: A family in Ohio insured two cars together. Thanks to the multi-car discount, each vehicle’s rate was about 12% lower than it would have been if insured separately. Car insurance plans

Always ask your agent or use an online calculator: those often show which discounts you qualify for. Saving on car insurance usually comes down to finding all the applicable discounts.

Specialised Car Insurance Plans?

Beyond standard policies, there are specialised car insurance plans for particular needs or partnerships. Here are some noteworthy types:

Student Car Insurance Plans

Student car insurance plans typically refer to car insurance policies for young or college drivers. Insurers often market to students, especially those living off-campus. Key points:

- Good Student Discounts: Many insurance companies automatically apply a discount if a student (teen) maintains good grades. This can save around 10% or more.

- Dependent Addition: Often, a college student can be added to a parent’s policy with minimal extra cost, especially if they don’t have their own vehicle. For example, if a student occasionally drives the family car, keep them on the parents’ multi-car policy to save money. Carr insurance plans

- Named Non-Owner Policies: If a student doesn’t own a car but sometimes drives others’ cars, they can get a non-owner policy. This isn’t a complete “car insurance plan” with comprehensive or collision, but it provides liability coverage when driving a borrowed car.

- Shopping Around: Rates for student drivers vary widely. Compare quotes specifically for students – some insurers (like GEICO or State Farm) have special student pricing.

Stat: A LendingTree study found teen drivers with good grades save ~$546 per year (10.9%) on premiums. That’s a significant saving, showing the value of this discount in student car insurance plans.

Family Car Insurance Plans

A family car insurance plan is not an official term, but it generally refers to covering multiple family members and vehicles under a single policy or insurer. Here’s how it works:

- Multi-Car Policies: As mentioned, insuring 2+ cars on a single policy earns a discount. All drivers living in the household get a break per car.

- Adding Young Drivers: Adding a teen to the family policy can be cheaper than getting them a separate plan. Even if the teen owns the car, parents might add it to their policy to qualify for the multi-car discount.

- Multi-Policy Bundles: Families often bundle home + auto insurance with one company to save even more. Car insurance plans

- Affordability: Generally, a family plan is more affordable per vehicle than separate policies. However, note that a claim on one car (or one driver’s accident) can raise rates for the whole policy, affecting the family.

When considering a family car insurance plan, always list all eligible cars and drivers to get full credit for discounts. Progressive clarifies that adding any eligible family or household member’s car yields a multi-car discount.

Roadside Assistance Car Insurance Plans?

Many insurers offer an optional add-on called Roadside Assistance. This isn’t mandatory, but it can be lifesaving in emergencies. With this add-on, if your car breaks down, the insurer will pay for: a car insurance plan.s

- Towing to the nearest repair shop or home

- Jump-starting a dead battery

- Changing a flat tyre (if you have a good spare)

- Fuel delivery (if you run out of gas)

- Lockout service (if you lock keys in the car, up to a limit)

- Winching (if you get stuck off-road or in snow)

According to Car and Driver, “almost all insurance companies provide roadside assistance plans as an add-on to your car insurance policy”. It’s true – carriers know it’s a popular extra.

Cost: It’s usually cheap. For example, GEICO offers 24/7 roadside assistance for “as little as $14 a year per car.” That’s barely more than $1 a month! Considering the cost of towing or emergency service, it’s often worth it for peace of mind.

Tip: Check what your car comes with. Some credit cards or auto clubs (such as AAA) include free roadside assistance. If you already have it elsewhere, you may skip the insurance add-on. Otherwise, the ~$10–$25/year per car is usually cheap insurance for any breakdown situation.

Luxe (Luxury) Car Insurance Plans?

“Luxe car insurance plans“ isn’t a standard industry term, but it implies coverage for high-end or exotic cars. Luxury and exotic vehicles have unique insurance needs: a car insurance plan.s

- High Value: A luxury car (Bentley, Ferrari, etc.) can cost hundreds of thousands of dollars. Some insurers (like Progressive) won’t insure cars over $150k, so owners of those vehicles use speciality insurers.

- Higher Premiums: Even modest sports cars have high rates because their parts and repairs are costly. Carrotypes with powerful engines also pose more risk. As a rule, the more expensive and performance-oriented the car, the higher its insurance premium.

- Agreed Value vs Actual Cash Value: Standard policies pay the actual cash value (depreciated). For rare or classic luxury cars, owners often want an agreed-value policy that guarantees a set payout if the vehicle is totalled.

- Collector or Classic Car Insurance: Sometimes, high-end car owners use classic car policies (if they don’t drive daily) to save money and insure at a declared value. But these have usage restrictions.

If you drive a luxury vehicle daily, talk to insurers that specialise in high-end auto. Companies like Chubb and Pure Insurance are known for luxury auto coverage (though they may only offer it as a bundle with a home policy, as many high-net-worth companies do).

Example

Chubb’s site says: “Whether you drive a luxury car, sports car, or an SUV, [our] auto insurance puts your safety first.” They market to high-end owners. In our research, Forbes lists insurers like Progressive and Travellers as top luxury car insurers, with average quotes of $3,300–$3,800/year for exotic cars. That’s several times the average policy, reflecting the higher risk and value of these cars.

Walmart Car Insurance Plans?

You may have heard of Walmart car insurance plans. Walmart itself does not underwrite insurance, but through partnerships, it offers car insurance quoting. Here’s how it works: an auto insurance plan

- Partnership Model: Walmart partnered with major insurers (such as GEICO, Allstate, and Progressive) to provide quotes on Walmart.com or in-store kiosks. This allows customers to get insurance while shopping.

- Potential Savings: A review found that Walmart’s insurance partners can offer competitive rates. In one state, a consumer saved up to 15% on premiums by choosing one of Walmart’s partner plans. The user entered their ZIP code on Walmart’s site and compared partner quotes.

- Convenience and Misconceptions: The idea is convenience; why not shop for insurance while you’re already shopping? However, coverage isn’t limited or inferior. As DIY Enthusiasts notes, Walmart’s partnered plans “offer the same level of coverage and customer service as other providers.” The only difference is that you access it through Walmart’s platform.

- Who Can Use It: Despite myths, anyone can compare these quotes. You don’t have to be a Walmart shopper or member. It’s a co-branding of existing insurers.

In summary, Walmart car insurance plans are simply quotes from big insurers, marketed through Walmart channels. It’s another way to compare auto insurance. If you find a lower quote through Walmart’s partners, great—remember, you’ll still buy from the insurer, not Walmart. Car insurance plan.s

Other Speciality Plans

Some other examples (less common) include:

- Commercial Auto Insurance: If you use your car for work (deliveries, rideshare, etc.), you need a business auto policy.

- Classic/Antique Car Insurance: For vintage cars, typically lower premiums if driven sparingly.

- Usage-Based Insurance (UBI): Some insurers offer pay-per-mile or telematics plans where safe driving earns significant discounts.

Each of these is a form of car insurance plan, tailored to specific needs. Always discuss your situation (student driver, family, high-value car, business use, etc.) with an insurance agent to get the right plan.

Affordable Car Insurance Strategies?

Finding affordable car insurance plans is a significant goal for most drivers. Here are 10 tips and strategies to save money:

- Compare Quotes Regularly: Rates change often. Use online comparison tools or work with an agent to get quotes from multiple insurers each year. Even a 5-10% difference can add up to significant savings on a $1,000+ premium.

- Bundle Policies: If you have homeowners or renters insurance, bundle it with your auto insurance. Discounts can range from 2% to 10%. For families, bundle all cars on one policy for multi-car discounts. Car insurance plan.s

- Choose a Higher Deductible: If you can afford the out-of-pocket cost, raising your deductible from $500 to $1,000 can lower your premiums noticeably. Only do this if you have emergency savings.

- Look for All Discounts: As listed above, ask about every discount you might qualify for: good student, safe driver, multi-car, home ownership, military, anti-theft devices, etc. Even a small 5-10% off helps.

- Maintain Good Credit: In most states, insurers use credit-based scores. Maintain good credit to keep premiums lower.

- Drive Safely: A clean record is a good thing. Avoid tickets and accidents. For teens, consider taking driver’s ed courses approved by insurers to earn additional discounts.

- Limit Mileage: If you can carpool or telecommute, reduce your annual mileage. Ask insurers about low-mileage or pay-per-mile programs for extra savings.

- Consider Usage-Based Insurance: Some companies offer programs in which a device monitors driving behaviour (speed, braking, etc.) and offers discounts for safe driving. If you’re a careful driver, this can reduce your rate.

- Maintain Continuous Coverage: Gaps in insurance (going uninsured) can lead to higher rates later. Always keep at least the state-required minimum to avoid insurer surcharges.

- Review Coverage Needs: If you have an older car (worth less than $5K), it might not make sense to pay for comprehensive or collision; you could drop them and save. Likewise, remove unnecessary extras (such as rental car reimbursement) if they are not needed.

By combining these tactics, many drivers find affordable car insurance plans that still provide the coverage they need. For example, checking quotes via Walmart’s partners or aggregator sites could reveal new discounts. Also, leveraging data: The Zebra’s reports show average U.S. premiums at $1,759, which can seem high. But with the above strategies, many pay below that average.

Navigating Confusing Insurance Terms?

Insurance jargon and similar-sounding terms can confuse consumers. Here are a few clarifications to keep in mind:

- Car vs. Health Insurance: Phrases like “Affordable Care Act insurance plans”, “Florida Health Care Plan insurance”, or “Fidelis Care insurance plans” all refer to health insurance, not auto insurance. Please don’t mix them. For context, Fidelis Care is a New York health insurer covering “more than 2.5 million… people “. That’s entirely separate from auto policies. Always ensure you’re looking at auto insurance information, not healthcare.

- No “Free” Car Insurance: Some ads or partners (like Walmart) might imply that there are deals. But remember, coverage costs money. A “cheap” quote usually means a higher deductible or lower coverage limit. Always read the fine print. As DIY Enthusiasts notes, Walmart’s car insurance options “offer the same level of coverage and customer service as other providers,” just through a different channel. Plans.

- Shop Smart, Don’t Switch Blindly: A “great deal” in one state or situation may not translate to another. For example, if you move from Ohio to New York, rates change drastically. Always get a fresh quote for your specific location and vehicle.

- Policy Period: Some confuse “annual” vs. “6-month” policies. Auto loan policies are typically 6 or 12 months. Make sure you know the period: a 6-month policy for $1,000 means $2,000/year.

- State Names in Insurance: Terms like “Florida Personal Injury Protection (PIP)” apply to auto only in Florida (or other no-fault states Don’t confuse that with the Florida Health Care Plan The latter is a state-administered health plan for low-income residents If you search for “Florida health care plan insurance” expecting auto info, you’ll get health coverage info instead.

In general, always double-check what you’re reading or quoting. If you see “plans” in an insurance context, identify whether it’s auto, health, home, etc. The strategies in this article specifically apply to auto insurance plans.

How to Choose the Best Car Insurance Plan?

Picking the right car insurance plan means balancing coverage and cost based on your needs. E e’sss a step-by-step approach:

- Assess State Requirements: First, understand your state’s minimum coverage requirements, and make sure you meet or exceed them (e.g., liability, PIP).

- Evaluate Your Needs: Consider your car’s value and usage. O, a new vehicle, full coverage (liability, collision, and comprehensive) is wise. O for an older car, drop collision coverage. Think about personal needs, too: Do you need rental car reimbursement or extra personal injury coverage?

- Set Your Budget: Decide on a deductible you can afford. Also, determine how much premium you’re comfortable paying.

- Gather Information: Write down car details (make/model/year), personal info (age, driving history), and coverage. Instead, provide your current policy info if you have one.

- Compare Quotes: Use online tools or agents to get multiple quotes. Make sure to compare the same coverage levels. Pay attention to the out-the-door price (not just the advertised rate).

- Check Discounts: Inform insurers of all possible discounts (education, safety features, association memberships, etc.) to ensure they apply them.

- Read Policy Details: Before buying, review exclusions and limits. For example, check whether the insurer covers rental car damage or whether a separate company provides roadside assistance.

- Ask Questions: If anything is unclear (e.g., “What does my uninsured motorist coverage limit mean?”), Contact a representative for clarity.

- Look at Insurer Reputation: Customer service and claim satisfaction matter. Check review ratings for the ones you’re considering.

- Review Annually: Once you have a good plan, review it annually. Life changes (moving, adding drivers, buying new cars) can affect your needs.

Call to Action: Now is the time to act. Get a quote today from several carriers (many offer instant online quotes). Compare them carefully, and don’t hesitate to negotiate or switch providers if a better deal is found.

Share and Save: This guide helps you navigate car insurance plans. Please share it on social media to help friends and family find the best coverage. Have questions or experiences with finding affordable car insurance? Leave a comment below—we’d love your tips!

Frequently Asked Questions (FAQs)

A car insurance plan can cover liability for damage you cause, collision damage, comprehensive losses (theft, storms), medical bills, and uninsured/underinsured motorist incidents. Overage ends on your policy selections.

The average U.S. car insurance premium is about $1,759/year, but costs vary widely by state, driver, and car. Some cities: $6,000/year; others: < $900/year. Factors: coverage levels, driving record, and location.

Student car insurance plans cover young or student drivers. Discounts apply (good student discount). Often, our parents’ policies are too costly.

Roadside assistance covers emergency services such as towing, jump-starts, fuel delivery, and lockout assistance. Most insurers offer it for a small fee.

No official “family plan”, but insuring multiple cars under one policy qualifies for discounts. Eenscan can also be added to the family policy to save on costs.

Share and Save: This guide helps you navigate car insurance plans. Please share it on social media to help friends and family find the best coverage. Any questions or experiences with finding affordable car insurance, leave a comment below. We’d love to hear your tips!

Call to Action: Ready to get a quote or contact an agent today? By pairing options and applying these tips, you’ll secure a car insurance plan that fits your budget and keeps you safely covered on the road.